Life insurance is essential for everyone but is only sometimes taught in schools or colleges. Most people, except a few top investors, need help understanding the industry. This article from the series will help you learn about the life insurance industry and make better equity investment decisions.

What is Insurance?

Insurance is a contract where one party (the insurer) promises to pay another party (the insured or beneficiary) a certain amount of money (the policy benefit) if a specific event happens. This is done in exchange for a payment (the premium).

Life Insurance vs. General Insurance

- Life Insurance: Utilizes actuarial science to assess risks and calculate premiums. It provides long-term financial benefits, including payouts after death or at the end of a specified term.

- General Insurance: Utilizes scientific principles to give funds for medical expenses or property damage, cover short-term risks, and pay for hospital bills or car repairs.

Key Concepts in Life Insurance for Investors

- Risk Pooling: Spreading individual risks across many people to reduce the impact of losses and make returns more stable.

- Law of Large Numbers: Combining many risks reduces the uncertainty of losses, making the insurer’s earnings more predictable.

Comparing Life Insurance and Banking

- Banking: Banks collect money from depositors and lend it out, earning profits from the difference in interest rates. They are vulnerable to economic changes.

- Life Insurance: Insurers collect premiums, invest them, and pay out benefits when needed. Profits come from the difference between investment returns and payouts, creating a stable revenue stream.

Stability in Insurance Pools

Unlike banks, where all depositors can withdraw money simultaneously, life insurance policies can’t be cashed out immediately. This stability allows insurers to plan investments better and manage risks more efficiently.

Important Terms for Investors

- Insurer: The company providing insurance.

- Insured: The person covered by the policy.

- Loss: Reduction in the value or quality of an insured item or person.

- Premium: Payment made by the insured to the insurer for coverage.

- Policy: The contract outlining insurance terms.

- Claim: A request for payment based on policy terms.

- Reinsurer: A company that takes on part of the risk from another insurer, spreading the risk.

Risk Management in Insurance

- Pure Risks: Only involve the possibility of loss and are insurable, offering stable returns (e.g., life or health insurance).

- Speculative Risks: Involve the likelihood of both loss and gain and are not insurable (e.g., stock market investments), leading to higher variability.

Ways to Manage Risk:

- Risk Avoidance: Avoiding activities that could cause loss (e.g., abstaining from smoking)

- Risk Reduction: Minimizing potential impacts, making returns more predictable (e.g., regular health check-ups).

- Risk Retention: Accepting and planning for financial impacts (e.g., paying a deductible)

- Risk Transference: Shifting risk through insurance creates stability (e.g., obtaining comprehensive auto insurance)

Types of Life Insurance Products:

Life insurance products are divided into:

- Protection Plans: Cover specific risks, like term insurance paying out on certain events.

- Savings Plans: Combine savings with insurance, offering growth and protection.

- Retirement/Annuity Products: Provide income during retirement, ensuring steady long-term returns.

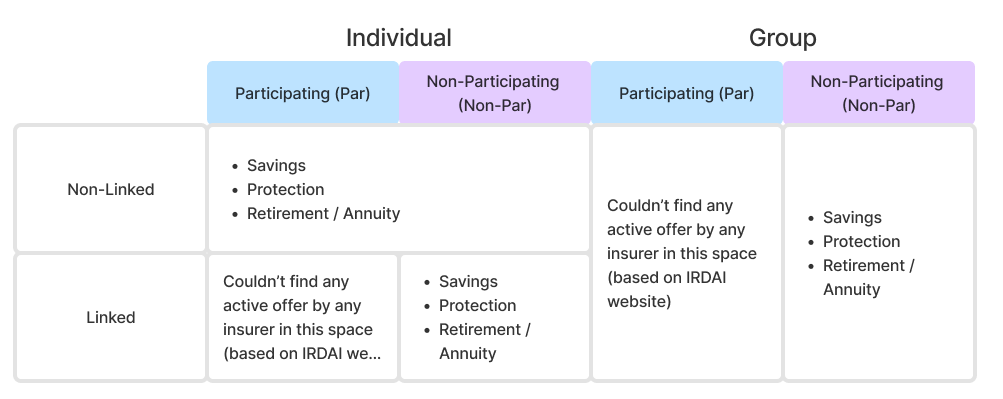

Key Business Segments of Life Insurance Companies

Life insurance products are also grouped by profit participation and investment linkage:

Participating (Par) Policies

- Features: Share in the insurer’s profits through dividends, offering extra returns.

- Returns Distribution: 90% to policyholders, 9% to shareholders, and 1% to the fund.

- Products: Savings, protection, retirement, and annuity.

Non-Participating (Non-Par) Policies

Features: Fixed benefits without profit-sharing, ensuring predictable returns.

Savings Products

- Individual Savings: Includes endowment and variable insurance plans linked to benchmarks.

- Immediate Annuity: Provides immediate income, ideal for regular payouts.

- Group Savings: Fund-based insurance for managing employee benefits like gratuity.

Protection Products

- Individual Protection: Offers guaranteed benefits for specific risks, such as death or critical illness.

- Group Protection: Provides coverage to groups, often used by employers for employees.

Unit-Linked Products (ULIPs)

- Features: Combines investment and insurance. Returns are tied to fund performance, offering higher potential returns.

- Products: Include savings, protection, retirement, and annuity options.

Realm of Possibilities

As the market matures, new product innovation continues to occur. However, offered products must belong to one of the following sub-categories:

Product Suite

Based on life insurance products and different segments, insurers offer various “basic” product suites, with continuous innovation for better market adoption:

- Protection Plans: Offer life coverage, secure financial goals, and protect the family.

- Insurance Plans with Savings: Provide financial growth while offering life coverage.

- Child Plans with Insurance: Ensure financial security for a child’s future, offering traditional and unit-linked options.

- Insurance Plans with Wealth Creation: Offer market-linked returns and life insurance coverage such as ULIP, etc.

Trends and Innovations

The life insurance industry continuously evolves, driven by changing consumer needs and economic conditions. New products and investment strategies are regularly introduced, offering diverse opportunities for investors.

Margin of Safety

Three hypotheses may explain why prominent investors like Warren Buffett might be cautious about investing in life insurance:

- Longevity Risk:

- Most life insurance plans span multiple decades, making it challenging to predict long-term mortality rates. Unexpected events like the COVID-19 pandemic can disrupt projections.

- Risk/Reward Dynamics:

- While life insurance generates a steady stream of premiums, Life insurers must avoid long-term investments in high-return assets to prevent asset-liability mismatches.

- As per the IRDAI website and analysis of the top 3 private insurers, 10-12% of the claims are death claims, 10-12% are towards planned benefit payout, and 65-70% payout is towards premature surrender, withdrawals, or discontinuance. This means that the bulk of the inflow cannot be invested in long-term high-return generating assets. Instead, significant portions of their inflows are allocated to government securities, bonds, and money market instruments, leading to modest net margins (7-8%).

- Property and Casualty (P&C) insurance can often achieve better returns with shorter duration policies and premium adjustments for different risk levels.

- Growth rate

- While the U.S. life insurance market shows limited growth due to widespread coverage and slow population growth, the Indian market has significant potential. With low insurance penetration, Indian life insurance companies have experienced 20-25% compound annual growth rates (CAGR) in the past decade and are projected to grow at 15-20% in the coming years.

For Warren Buffett, it might be prudent to invest in P&C companies. However, equity investors targeting the Indian market, where the P&C insurance market is still evolving with a growing focus on Life Insurance at the retail level, should analyze and find a good investment opportunity in the current decade.